4th Quarter 2019 Market Update

Summary

- Coming into 2019, markets were being priced for a recession which did not occur. However, multiple expansion throughout 2019 occurred on the back of the Federal Reserve unwind of 3 rate cuts and liquidity injections into the repo market while earnings have been flat.

- From a long term perspective, stocks have continued to advance as most of the major headwinds involving the U.S.-China trade deal have come to a close as a comprehensive phase one deal has been reached. Hopes of an earnings rebound are being priced into stocks.

- A combination of an accommodative Federal Reserve, and trade deal concerns dissipating allowed investors to rotate from a defensive mind-set and into more of a risk on approach as confidence returned.

- As long as the Fed keeps interest rates low, and continues to provide liquidity, this would favor growth over value as this has been a continued trend from the past 5 years.

Conclusion: With the major run up in stock prices this has expanded company’s valuations off relatively flat earnings. 2020 will be a year of either living up to these high expectations or falling short, forcing investors to rethink their bullish mood despite an accommodative Fed.

4th Quarter Highlights - What do I need to know?

- Markets started to gain upside momentum after a relatively flat previous quarter

Technical Market Assessment:

- This is our Long-Term market indicator that takes 20 technical factors into account and through a statistical process creates an overall score.

- As the S&P continued to make new highs, so did our RCI indicator which hit levels of 90 during its latest breakout to new highs. This is a strong momentum indicator with price entering a new territory.

- We closed out the year with a reading of 75 which is still a great score.

Big Picture on Markets:

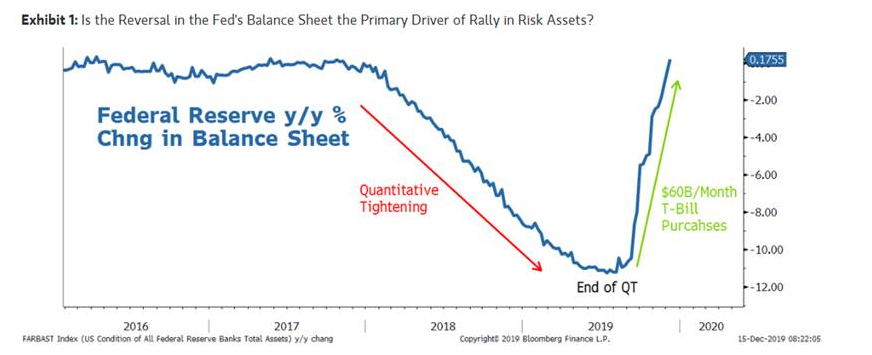

- Since the beginning of October you can see that the trend in the S&P has remained strong. Once we got above the technical breakout and psychological level of 3000 the momentum began to carry over. Note that Fed began $60b in monthly treasury bills to keep interest rates low starting October 15th (coincidence?).

- The Russell 2000 (small capitalization index) has underperformed the S&P 500 all year while also being stuck sideways trading range. Recently, small caps have joined in on the rally alongside large caps and broken out of this range. This is a positive technical development.

- As we look at emerging markets ex U.S. we can also see that EM markets have followed developed markets. They have underperformed, but are finally starting to show some signs of a longer term uptrend after being sideways for some time. The U.S. Dollar trajectory will hold the key on future EM direction.

Big Picture Market Summary:

- As it has been the case all year, the large cap S&P 500 index has been your leader. A small group of just five stocks in the S&P 500 have produced the majority of the indexes gains. Passive indexing that is non-agnostic on which stocks get bought continues to push up the values of the highest market cap stocks. For this reason diversified client portfolios may have under-performed when compared against the S&P 500.

- Long term trend is up; however, we are on a short-term unsustainable trajectory. At present, the risk of a pullback in the short term is large. Risk/Reward over the next quarter maybe unfavorable. Earnings will need to meet high expectations.

- Small Caps have largely under-performed. It would be a positive technical development if small caps can start to play catch-up to the S&P 500.

- We believe that the value stock repricing that happened in the 3rd and 4th quarter is mostly over. Growth stocks should continue to lead as long as the Fed stays accommodative and continues liquidity injections. Valuations of those growth stocks are another matter.

- Developed international and emerging markets have spent the last decade under-performing its U.S. counterpart. We eagerly await relative strength in this area as investors are hoping this recent rally is the start.

Sectors showing relative strength in the 4th Quarter:

- Semiconductors have without a doubt been the leading sector in the market. Semi’s drastically outperformed the S&P and has continued to be a coinciding indicator for where overall markets move.

- With help from the semiconductors, the tech sector continues to lead the S&P index higher. Tech and the sub sectors within have been by far the best performers throughout the year.

- Financials outperformed the S&P as further rate cuts combined with a slight pickup in yields have given investors some hope money can be made here.

Here are the sectors that underperformed:

- Long term treasuries have continued to decline with yields moving higher in the quarter. This is also a part of the defensive trade unwinding its substantial gains throughout the year.

- While real estate helped lead most of Q3 with its sensitivity to interest rates, it began to underperform as some of the cuts were priced in and defensive positioning started to unwind.

Takeaways:

- Advisors should be aware of the outstanding performance of every single asset class, which is a rare occurrence. Going forward into a new year we have to be aware of these out-performances and be able to not become complacent with diversification. While it might be tempting to ramp up equity exposure or cut out hedges like gold, sticking with a diversification strategy should remain a top priority. The temptation to fall victim to recency bias is relatively easy with the outstanding performance of everything as a whole, but while these types of returns across the board have been seen before, it should be noted that this shouldn’t be an excuse to throw diversification out the window.

Risks to Bonds Remain

- The risk for bonds remains a threat for allocation of portfolios. The main objective for bonds during 2019 was for capital appreciation and not income. With equities at all-time highs and yields starting to show signs of bottoming, the risk for the typical 60/40 portfolio is rather dramatic as a large decline in equities could not be offset with an increase in bond prices. The typical diversification might not have a positive expected return if momentum starts to shift in the opposite direction and yields continue their rise and equities fall from their historic levels.

What is the news driving markets and Investor perceptions?

Fed Liquidity, Algo’s & Perception = Multiple Expansion

- A major driver of performance in Q4 comes on the backing of the expansion of the Feds balance sheet. Since the fears in the repo market in September the Fed began to inject liquidity into the market ensuring the borrowing and lending capacity of major banks.

- Loosening the squeeze on cash allows investors to be more aggressive and allocated to risk assets and typically this will benefit longer dated risk assets such as Growth stocks.

- Algorithmic traders and quants also seemed to be keyed in on what is perceived to be excess liquidity by the Fed creating a positively correlated feedback loop to Fed balance sheet and the S&P 500.

A Year to Remember

- 10 out of the 12 months in 2019 were all green. We had two noteworthy pull backs throughout the year in May & August which were both trade war related events.

- While the beginning of the year is a bit skewed because of the end of the year drop off last year, the performance since October has been substantial, taking out new highs along the way.

- The Santa rally came to fruition as we added to our gains as we closed out the year.

Easy Money

- The common theme around the world has continued to be monetary easing around the globe with banks around the world continuing to cut interest rates.

- Most of the Central Banks around the world have low interest rates and some actually have negative interest rates. This low rate environment puts a bit more pressure on the U.S. which has some of the highest interest rates globally.

- With still room to cut the Fed will continue to debate whether or not more cuts in 2020 are warranted, or if they need to see slower growth in order to use some of their extra ammo to stimulate the economy.

Earnings Playing Catch Up?

- While the 4th quarter S&P EPS declined, the price of S&P continued to rise, and now that some of these stocks are trading at higher multiples the question is if these companies earnings will start to pick back up after the recession fears have diminished

- Now this begs the question, is this appreciation a direct result of the fed’s liquidity, or will the reduction of tariffs and trade tensions actually start to improve company’s bottom lines, capital expenditures, and CEO confidence?

Fundamentals Diverging

- Along with divergence between earnings growth and S&P price appreciation, there is further divergence between the ISM Composite PMI numbers which continued its decline in manufacturing activity as new orders, production, employment and new export orders are shrinking at a fast pace while the market doesn’t seem to mind and continues to rally.